By: Jon Schultz, CPA and Kimberly Haynes, CPA

In-kind gifts have traditionally been an important source of support for colleges, schools and other education-focused nonprofits. Contributed non-financial assets have also posed problems for organization leaders, who have sometimes struggled to comply with tax reporting rules. Accounting Standards Update (ASU) 2020-07 ups the challenge factor by revising the regulatory requirements for presentation and treatment of these resources. Are you ready?

The update’s full name is Accounting Standards Update (ASU) 2020-07, Not-For-Profit Entities (Topic 958): Presentation And Disclosures By Not-For-Profit Entities For Contributed Nonfinancial Assets. That complex nomenclature belies a simple goal: increasing transparency around in-kind gifts to communicate the organization’s relative efficiency more accurately.

What’s covered

The new reporting rules cover all types of contributed nonfinancial assets, including many that are frequently given to (and appreciated by) educational institutions.

- Fixed assets such as buildings, equipment and land

- Supplies

- Materials

- Food

- Clothing

- Services

- Utilities

- Use of facilities

- Intangible assets

Under the updated regulations, organizations must include in their financial statements detailed information describing the gifts as well as how they are used, how they fit into the overall budget and how they contribute to the recipient’s nonprofit mission. The information can be presented as a table, in narrative form or through a combination of both.

What’s different

ASU 2020-07 lays out basic requirements for presentation and disclosure that differ from previous standards. First, nonprofits must present nonfinancial asset contributions as a separate line item in the Statement of Activities. This entry is only for nonfinancial contributions and must not include donations of cash or other financial assets (i.e. donated securities).

The updated standard also requires organizations to disclose all contributed nonfinancial assets disaggregated by category, clearly showing the amount and type of contributions received along with additional information about each category:

- Were the contributions used or monetized during the reporting period? If used, in which programs and activities?

- What is the organization’s policy for determining whether to utilize or monetize in-kind contributions?

- What donor-imposed restrictions apply to the contributions, if any?

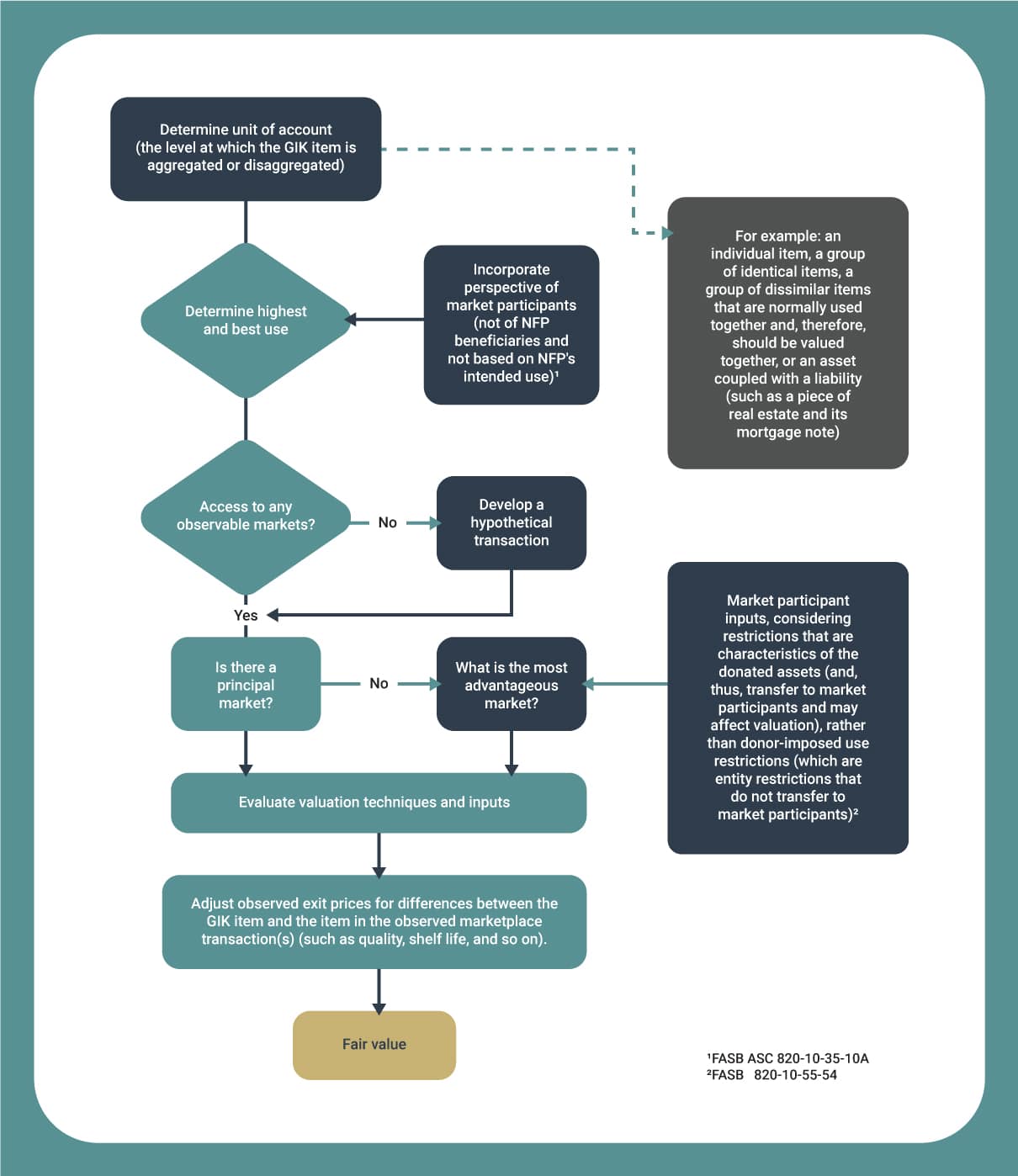

- Which valuation techniques and inputs did the organization use to determine initial valuation for the contributions?

- What is the principal market or most advantageous market the organization used to establish fair value of the in-kind contribution if donor-imposed restrictions prohibit the organization from selling or using the asset in that market?

The Financial Accounting Standards Board (FASB) issued ASU-2020-07 in September of 2020, effective for fiscal years beginning after June 15, 2021—or interim periods beginning thereafter June 15, 2022, for organizations with interim reporting policies. Organizations must apply the update retrospectively, and early adoption is permitted.

Key compliance strategies

Careful record-keeping is key to compliance. That’s doubly true for organizations that present comparative financial statements, which will need to track all relevant data regarding in-kind contributions from the beginning of the fiscal reporting period prior to the one in which the organization adopts the new standard.

While some nonprofits may already collect and track all of the required data points, many do not. It’s imperative for all NFPs to carefully review record-keeping processes and policies that apply to in-kind contributions, including donor restrictions. Leaders need to ensure that the appropriate data is being gathered and retained in a disaggregated form to enable compliance.

If existing procedures do not effectively capture all the required information, it’s important to adapt processes and adjust financial accounting systems and charts of accounts as needed —sooner rather than later, to avoid reporting crunch time headaches.

It’s also good practice to align program and activity names in all systems, so that this terminology matches between disclosures and expenses in the statement of activities (and everywhere else).

Who benefits from the new rules?

FASB’s goal in issuing ASU 2020-07 was increasing transparency around in-kind contributions so that donors, grantors, regulators and others could more easily determine where these gifts went and understand their true impact.

The new requirements hold the potential to benefit nonprofits as well, through enhanced clarity and new opportunities to encourage non-financial contributions. By effectively communicating information about the types and uses of in-kind donations, leaders can raise awareness of the value of this kind of giving and its importance to the organization.

Full compliance with the updated regulations for in-kind contributions is mandatory, but it also represents an opportunity for your organization. Be sure you understand the requirements clearly and devote serious thought to how you can not only follow the rules, but also create lasting benefit for the organization as you work to meet them. Your Mauldin & Jenkins advisor can help.

{kind=link}